From Rolling Quarters to Monthly Estimates: SIDRA Mensalization Guide

Source:vignettes/sidra-mensalization.Rmd

sidra-mensalization.RmdOverview

Brazil’s Continuous National Household Sample Survey (PNADC) publishes labor market indicators as rolling (moving) quarters — 3-month moving averages where each published “quarter” shares 2 months with its neighbors. This smoothing hides short-term dynamics: turning points are delayed, seasonal patterns are distorted, and international comparison becomes difficult.

The PNADCperiods package includes a SIDRA mensalization module that recovers exact monthly estimates from rolling quarter data. This vignette explains how to use it.

Why Rolling Quarters Are Problematic

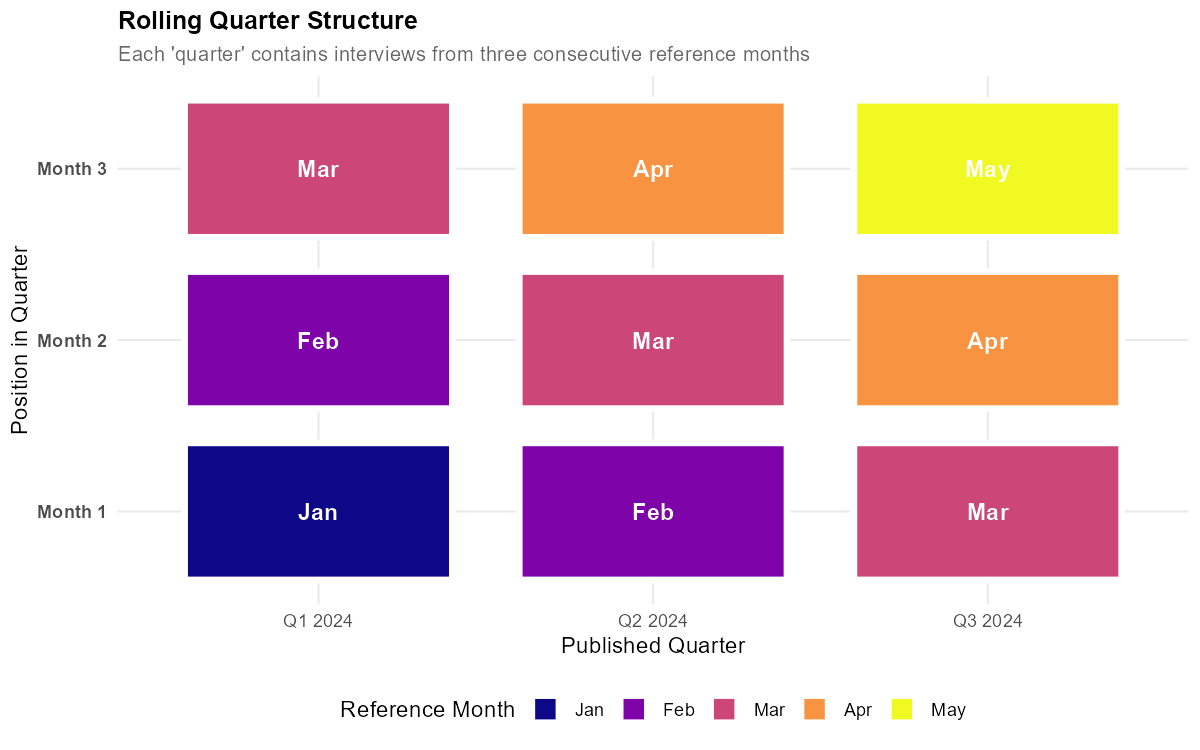

Each published “quarter” is actually a 3-month moving average:

- “2019-Q1” = average of Jan, Feb, Mar 2019

- “2019-Q2” = average of Feb, Mar, Apr 2019

- “2019-Q3” = average of Mar, Apr, May 2019

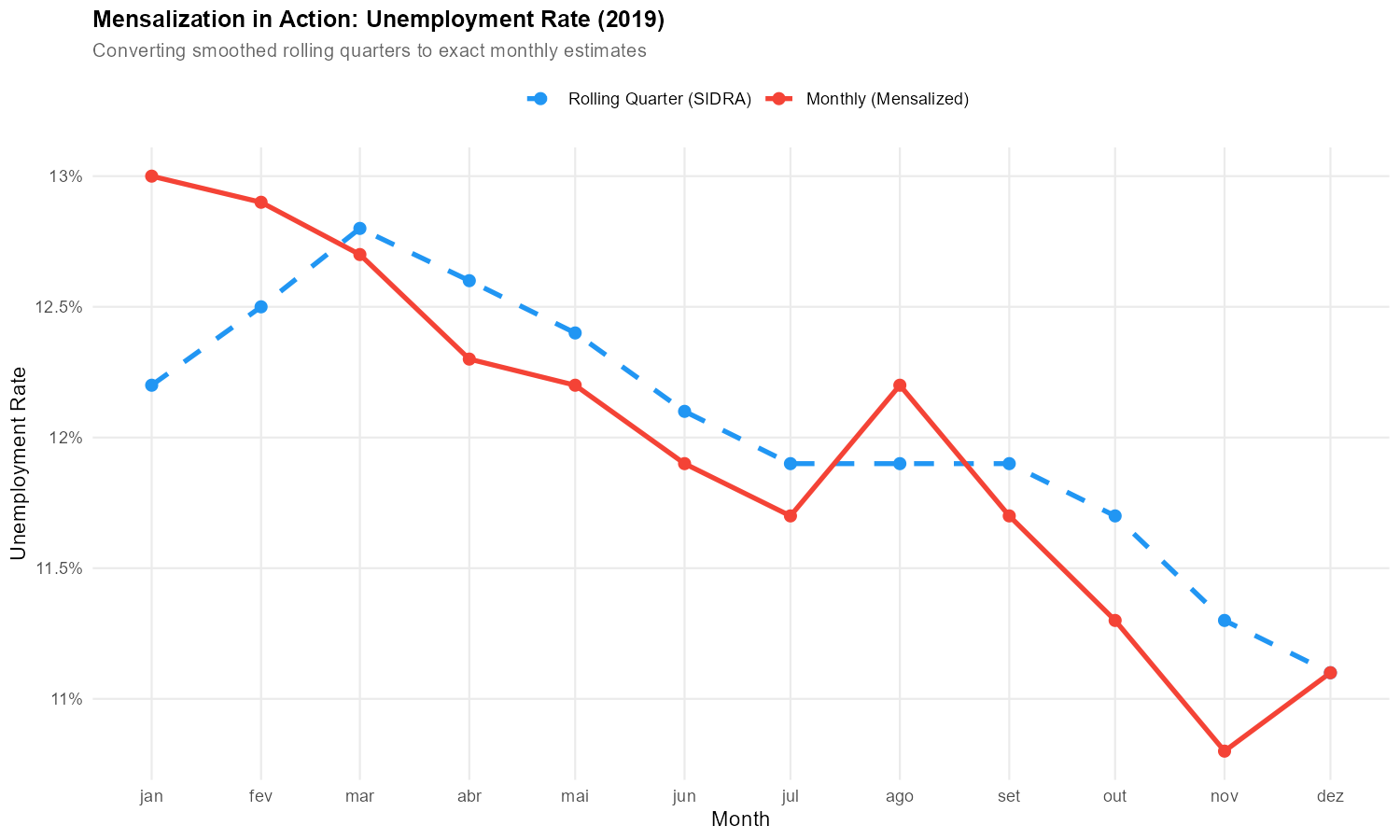

When unemployment jumps sharply in a single month, the rolling quarter spreads that spike across multiple overlapping periods. The mensalization algorithm inverts this averaging process to recover the true monthly values.

Quick Start

library(PNADCperiods)

# Step 1: Fetch rolling quarter data from SIDRA API

rolling_quarters <- fetch_sidra_rolling_quarters()

# Step 2: Convert to monthly estimates

monthly <- mensalize_sidra_series(rolling_quarters)

# Step 3: Use your monthly data!

head(monthly[, .(anomesexato, m_popocup, m_taxadesocup)])That’s it! You now have monthly estimates starting from January 2012.

fetch_sidra_rolling_quarters()downloaded 86+ economic indicators from IBGE’s SIDRA APImensalize_sidra_series()applied the mensalization formula using pre-computed starting points (bundled with the package)The result is a

data.tablewith one row per month andm_*columns for each mensalized series

Understanding the Output

The mensalized output contains:

-

anomesexato: Month identifier (YYYYMM format, e.g., 201903 = March 2019) -

m_*columns: Mensalized (monthly) estimates for each series - Price indices:

ipca100dez1993,inpc100dez1993(passed through for deflation)

Key series include:

| Column | Description | Unit |

|---|---|---|

m_populacao |

Total population | Thousands |

m_pop14mais |

Population 14+ years | Thousands |

m_popocup |

Employed population | Thousands |

m_popdesocup |

Unemployed population | Thousands |

m_taxadesocup |

Unemployment rate | Percent |

m_taxapartic |

Labor force participation rate | Percent |

m_massahabnominaltodos |

Total nominal wage bill | Millions R$ |

Rate series (like m_taxadesocup) are

derived from mensalized level series when

compute_derived = TRUE (the default). They are computed as

ratios of the mensalized levels, not directly mensalized from the

rolling quarter rates.

Discovering Available Series

Use get_sidra_series_metadata() to explore all 86+

available series:

meta <- get_sidra_series_metadata()

# View series organized by theme

meta[, .N, by = .(theme, theme_category)]

# Filter to specific theme categories

meta[theme_category == "employment_type", .(series_name, description)]The metadata uses a hierarchical taxonomy: theme (top

level, e.g., “labor_market”), theme_category (e.g.,

“employment_type”), and optionally subcategory (e.g.,

“levels”, “rates”).

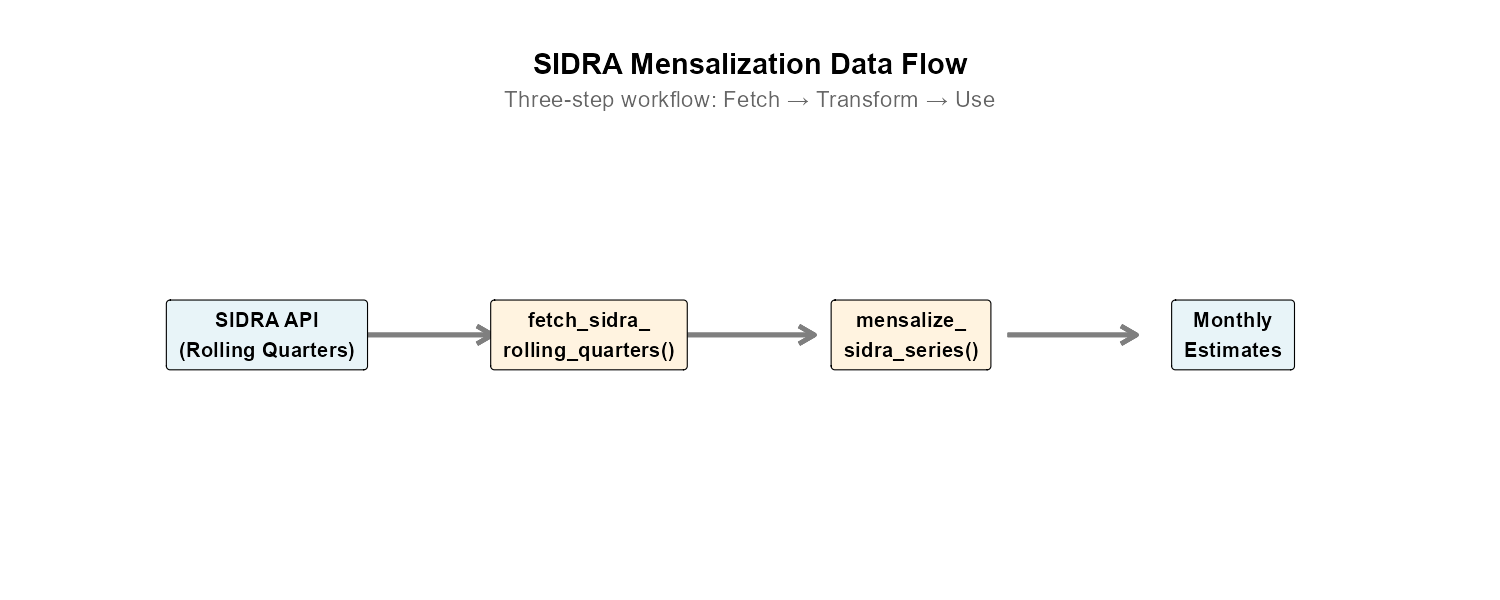

Data Flow

The mensalization process follows a three-step pipeline:

Step 1: Fetching Rolling Quarter Data

fetch_sidra_rolling_quarters() downloads data from five

SIDRA tables:

| Table | Content |

|---|---|

| 4093 | Population and labor force |

| 6390 | Income (nominal and real) |

| 6392 | Real income by occupation |

| 6399 | Employment by sector |

| 6906 | Underutilization indicators |

rq <- fetch_sidra_rolling_quarters(verbose = TRUE)

# Inspect structure

dim(rq)

names(rq)[1:20]Key columns: anomesfinaltrimmovel (end month of rolling

quarter, YYYYMM), mesnotrim (month position 1/2/3), plus

one column per series.

Step 2: The Mensalization Transform

monthly <- mensalize_sidra_series(rq, verbose = TRUE)

# Compare dimensions

cat("Rolling quarters:", nrow(rq), "rows\n")

cat("Monthly data:", nrow(monthly), "rows\n")The row count is approximately the same (one per month), but the meaning changes from “rolling quarter ending in month X” to “exact estimate for month X”.

Step 3: Using Monthly Estimates

Show plotting code

# --- VIGNETTE CODE: plot-unemployment ---

library(ggplot2)

monthly[, date := as.Date(paste0(substr(anomesexato, 1, 4), "-",

substr(anomesexato, 5, 6), "-01"))]

ggplot(monthly, aes(x = date, y = m_taxadesocup)) +

geom_line(color = "#1976D2", linewidth = 0.8) +

labs(title = "Monthly Unemployment Rate",

x = NULL, y = "Unemployment Rate (%)")Population Data for Weighting

For analyses requiring monthly population estimates separately:

pop <- fetch_monthly_population()

head(pop)Returns a data.table with ref_month_yyyymm and

m_populacao columns.

Working with Series

Fetching by Theme

Instead of fetching all 86+ series, filter by theme or theme category:

# Only employment type series

employment <- fetch_sidra_rolling_quarters(theme_category = "employment_type")

# Only wage mass series

wages <- fetch_sidra_rolling_quarters(theme_category = "wage_mass")

# Only labor market theme (includes participation, unemployment, employment types, etc.)

labor <- fetch_sidra_rolling_quarters(theme = "labor_market")Fetching Specific Series

For maximum efficiency, request only the series you need:

# Only unemployment-related series

unemp <- fetch_sidra_rolling_quarters(

series = c("popdesocup", "taxadesocup", "popnaforca")

)Excluding Derived Series

Some series are rates computed from other series. To fetch only “base” series:

# Exclude computed rates (only population and income levels)

base_only <- fetch_sidra_rolling_quarters(exclude_derived = TRUE)Selecting Output Columns

After mensalization, select columns as needed:

monthly <- mensalize_sidra_series(rq)

# Select specific series

labor_market <- monthly[, .(

anomesexato,

employed = m_popocup,

unemployed = m_popdesocup,

unemp_rate = m_taxadesocup,

participation = m_taxapartic

)]The Mensalization Methodology

This section can be skipped by users who just need results.

The Core Concept

Rolling quarters are 3-month moving averages. If we denote the true monthly value for month as , then the rolling quarter value is:

The mensalization algorithm inverts this relationship to recover from the sequence of values.

The Mensalization Formula

Step 1: Compute first differences

Step 2: Identify month position (mesnotrim)

Each month has a position within its quarter: - Position 1: Jan, Apr, Jul, Oct - Position 2: Feb, May, Aug, Nov - Position 3: Mar, Jun, Sep, Dec

Step 3: Cumulative sum by position

For each position separately, compute the cumulative sum of first differences, starting from a calibrated “starting point” :

The Role of Starting Points ()

The starting point is crucial. It determines the level of all subsequent monthly estimates. The package includes pre-computed starting points for 53 series, calibrated during the stable 2013-2019 period.

Starting points are computed by:

- Processing PNADC microdata to get “true” monthly aggregates ( values)

- Comparing these to rolling quarters

- Finding the that makes match the microdata

Practical Considerations

API Caching

The package caches SIDRA API responses in memory during your R session:

# First call: fetches from API (~10 seconds)

rq1 <- fetch_sidra_rolling_quarters()

# Second call with use_cache = TRUE: uses cached data (instant)

rq2 <- fetch_sidra_rolling_quarters(use_cache = TRUE)

# Clear all cached data (force fresh fetch on next call)

clear_sidra_cache()The cache persists until you call clear_sidra_cache() or

restart R.

Common Errors

| Error | Cause | Solution |

|---|---|---|

| “Series not found” | Misspelled series name | Check get_sidra_series_metadata()

|

| “API timeout” | SIDRA server slow | Retry; use use_cache = TRUE

|

| “No starting points” | Custom series | See Custom Starting Points below |

# Check if series exists

meta <- get_sidra_series_metadata()

"taxadesocup" %in% meta$series_name # TRUEData Quality Notes

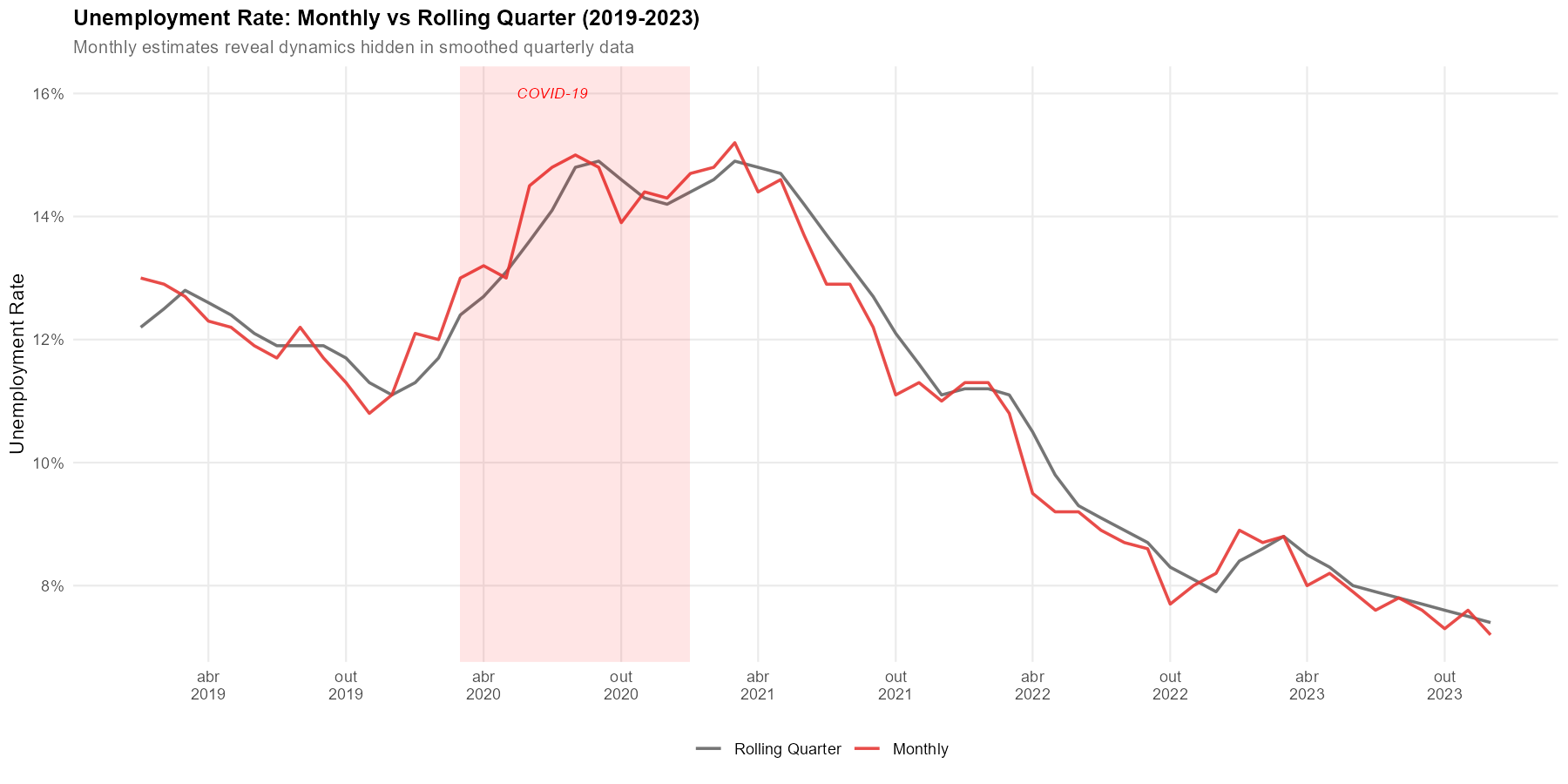

COVID-19 disruptions (2020): IBGE suspended in-person interviews during the pandemic. Some indicators show unusual patterns in 2020-Q2.

CNPJ series availability: Series based on CNPJ registration (empregadorcomcnpj, contapropriacomcnpj, etc.) are only available from October 2015, when V4019 was introduced.

Custom Starting Points

For users with calibrated PNADC microdata.

Use the bundled starting points (default) unless:

- Your series isn’t bundled — Custom variable definitions

- Different calibration period — Non-standard reference period

- Regional breakdown — State or metro-area mensalization

Option A: All-in-One Function

# Load your stacked PNADC microdata (with pnadc_apply_periods weights)

stacked <- readRDS("my_calibrated_pnadc.rds")

# Compute starting points

custom_y0 <- compute_starting_points_from_microdata(

data = stacked,

calibration_start = 201301L,

calibration_end = 201912L,

verbose = TRUE

)

# Use custom starting points

monthly <- mensalize_sidra_series(rq, starting_points = custom_y0)Option B: Step-by-Step

# Step 1: Build crosswalk and calibrate

crosswalk <- pnadc_identify_periods(stacked)

calibrated <- pnadc_apply_periods(

stacked, crosswalk,

weight_var = "V1028",

anchor = "quarter",

calibration_unit = "month"

)

# Step 2: Compute z_ aggregates (monthly totals from microdata)

z_agg <- compute_z_aggregates(calibrated)

# Step 3: Fetch rolling quarters for comparison

rq <- fetch_sidra_rolling_quarters()

# Step 4: Compute starting points

y0 <- compute_series_starting_points(

monthly_estimates = z_agg,

rolling_quarters = rq,

calibration_start = 201301L,

calibration_end = 201912L

)

# Step 5: Use custom starting points

result <- mensalize_sidra_series(rq, starting_points = y0)CNPJ-based series automatically use a later calibration period

(2016-2019) when use_series_specific_periods = TRUE (the

default in compute_series_starting_points()).

Validating Custom Starting Points

bundled <- pnadc_series_starting_points

# Merge and compare

comp <- merge(custom_y0, bundled,

by = c("series_name", "mesnotrim"),

suffixes = c("_custom", "_bundled"))

comp[, rel_diff := abs(y0_custom - y0_bundled) / abs(y0_bundled) * 100]

comp[rel_diff > 1] # Flag series with >1% differenceCase Study: COVID-19 Unemployment

How quickly did unemployment rise when COVID-19 hit Brazil? Rolling quarter data obscures these dynamics. Monthly estimates reveal the exact timing.

Show analysis code

# --- VIGNETTE CODE: covid-analysis ---

# Fetch all series and mensalize

rq <- fetch_sidra_rolling_quarters()

monthly <- mensalize_sidra_series(rq)

# Filter to COVID period

covid_period <- monthly[anomesexato >= 201901 & anomesexato <= 202212]

# Create date column

covid_period[, date := as.Date(paste0(

substr(anomesexato, 1, 4), "-",

substr(anomesexato, 5, 6), "-01"

))]

# Find peak

peak_month <- covid_period[which.max(m_taxadesocup)]

cat("Peak unemployment:", peak_month$m_taxadesocup, "% in",

format(peak_month$date, "%B %Y"), "\n")

Key findings from monthly estimates:

Exact peak timing: Monthly data pinpoints the peak month, while rolling quarters show only a gradual rise

Speed of impact: The monthly series reveals a sharp spike that rolling quarters smooth over 3+ months

Recovery dynamics: Monthly estimates show pauses and reversals in recovery that are hidden in quarterly averages

Series Naming Conventions

| Pattern | Meaning | Example |

|---|---|---|

m_ |

Mensalized monthly estimate | m_popocup |

pop* |

Population count |

populacao, pop14mais

|

*comcart |

With formal contract | empregprivcomcart |

*semcart |

Without formal contract | empregprivsemcart |

*comcnpj |

With CNPJ registration | empregadorcomcnpj |

taxa* |

Rate (percent) | taxadesocup |

nivel* |

Level/ratio (percent) | nivelocup |

rend* |

Income (rendimento) | rendhabnominaltodos |

massa* |

Wage bill (massa salarial) | massahabnominaltodos |

*hab* |

Usually received (habitual) | rendhabnominaltodos |

*efet* |

Actually received (efetivo) | rendefetnominaltodos |

For the complete catalog, use

get_sidra_series_metadata():

meta <- get_sidra_series_metadata()

# Filter by theme category

meta[theme_category == "employment_type", .(series_name, description)]

# Filter by theme and pattern

meta[theme == "labor_market" & grepl("taxa|nivel", series_name),

.(series_name, description)]Function Reference

| Function | Purpose |

|---|---|

fetch_sidra_rolling_quarters() |

Download rolling quarter data from SIDRA API |

fetch_monthly_population() |

Get monthly population estimates |

mensalize_sidra_series() |

Convert rolling quarters to monthly estimates |

get_sidra_series_metadata() |

Explore available series and metadata |

clear_sidra_cache() |

Clear cached API data |

compute_z_aggregates() |

Compute monthly aggregates from calibrated microdata |

compute_series_starting_points() |

Compute values from aggregates |

compute_starting_points_from_microdata() |

All-in-one computation |

Bundled data:

pnadc_series_starting_points — pre-computed

for 53 series x 3 month positions (calibration period: 2013-2019).

References

-

HECKSHER, Marcos; BARBOSA, Rogerio J. “Estimation of exact months for the microdata and rolling quarter series from PNAD Continua”. SocArXiv preprint, 2026. https://osf.io/preprints/socarxiv/fra5u_v1

Earlier formulations of the methodology:

- HECKSHER, Marcos. “Valor Impreciso por Mes Exato: Microdados e Indicadores Mensais Baseados na Pnad Continua”. IPEA - Nota Tecnica Disoc, n. 62. Brasilia, DF: IPEA, 2020. https://portalantigo.ipea.gov.br/portal/index.php?option=com_content&view=article&id=35453

- HECKSHER, M. “Cinco meses de perdas de empregos e simulacao de um incentivo a contratacoes”. IPEA - Nota Tecnica Disoc, n. 87. Brasilia, DF: IPEA, 2020.

- HECKSHER, Marcos. “Mercado de trabalho: A queda da segunda quinzena de marco, aprofundada em abril”. IPEA - Carta de Conjuntura, v. 47, p. 1-6, 2020.

Barbosa, Rogerio J; Hecksher, Marcos. (2026). PNADCperiods: Identify Reference Periods in Brazil’s PNADC Survey Data. R package version v0.1.2. https://CRAN.R-project.org/package=PNADCperiods

Further Reading

-

vignette("getting-started")— Setting up PNADC microdata analysis -

vignette("how-it-works")— The period identification algorithm -

vignette("applied-examples")— Applied research examples - IBGE SIDRA API: https://sidra.ibge.gov.br/

- Package repository: https://github.com/antrologos/PNADCperiods